Public Provident Fund (PPF): A Smart Yet Simple Strategy for Long-Term Wealth

INVESTMENTS

KishnaAgrawal

4/6/20263 min read

Understanding the Public Provident Fund (PPF)

The Public Provident Fund, commonly known as PPF, is one of the most popular long-term investment schemes endorsed by the Indian government. It serves as an excellent option not only for saving money but also for securing tax benefits. PPF offers a unique combination of safety, attractive interest rates, and tax exemptions, making it an ideal choice for investors looking to minimize their tax liabilities while building a substantial corpus over time.

Most young earners today chase high returns—but ignore stability. That’s where Public Provident Fund (PPF) plays a crucial role. It is not just a tax-saving tool; it is a foundation for long-term financial security.This blog will help you understand why PPF matters early, how it works, and whether it truly fits into your financial plan

Why PPF is Important at a Younger Age

Starting PPF early gives you a time advantage, which is more powerful than high returns.

Long Compounding Period: 15 years lock-in + extension option means your money grows continuously

Low Financial Pressure: Young earners can invest small amounts comfortably

Discipline Building: Lock-in prevents unnecessary withdrawals

Future Security: Acts as a backup fund for retirement or major life goals

👉 Simple Insight:

“Early start = More compounding = Bigger tax-free corpus”

How PPF Actually Works

(Basic Understanding)

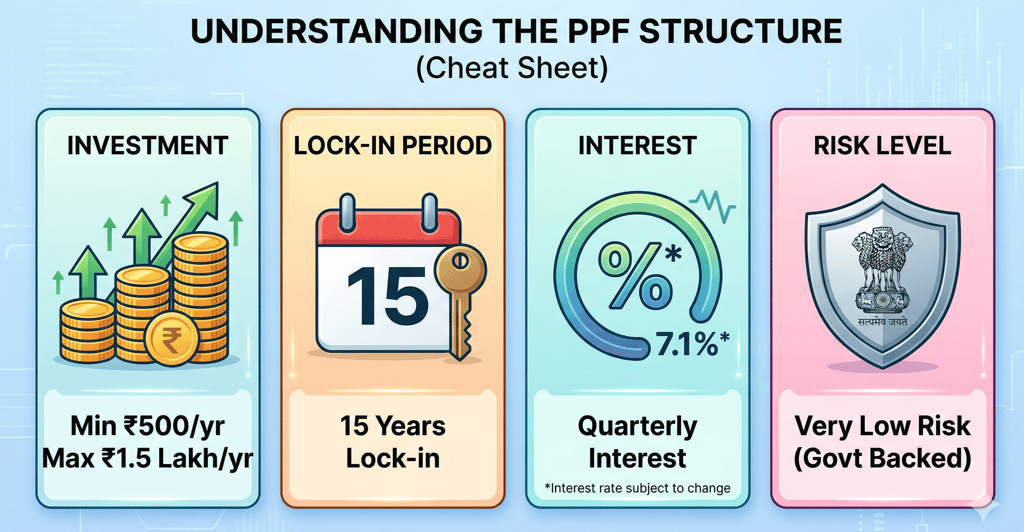

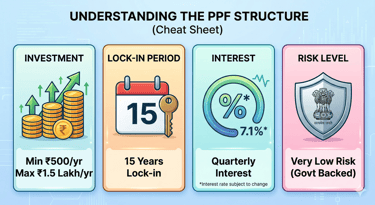

While numerous investment avenues are available, PPF stands out due to its unparalleled safety and assurance provided by the government. The investment is backed by the central government, ensuring that the principal amount remains secure. Furthermore, PPF offers a fixed interest rate that compounds annually, fostering wealth generation over a 15-year lock-in period. Unlike other options that may carry market risk, PPF guarantees returns, making it a safer harbor for your savings.

Moreover, PPF is flexible in terms of contributions, allowing investors to deposit a minimum amount of just ₹500 per financial year while capping the maximum at ₹1.5 lakh. This provides both small and large investors a chance to utilize PPF for tax saving effectively without straining their finances.

In conclusion, the Public Provident Fund is an exceptional investment vehicle that not only assists in tax savings but also encourages disciplined saving habits. For those seeking a reliable and profitable option, PPF should definitely be considered as a part of their financial strategy.

👤Example: Ravi (Age 25, Private Job)

Ravi, a 25-year-old salaried individual earning around ₹6.5 lakh per year, started his financial journey with a simple mindset—save tax, keep money safe, and avoid unnecessary risk. Like many people at this stage, he chose to invest ₹1 lakh annually in Public Provident Fund (PPF). In the initial 5 years, although his total investment reached ₹5 lakh, the visible growth was modest. At this stage, many people feel that returns are low, but Ravi was actually building something more important—consistent saving discipline and yearly tax benefits. By the 10th year, with ₹10 lakh invested, the impact of compounding started becoming noticeable. His money was growing steadily without any risk, and he had silently created a financial cushion for himself.

By the time Ravi completed 15 years, which is the maturity period of PPF, his total investment of ₹15 lakh had grown to approximately ₹25–27 lakh, completely tax-free. There was no stress of market fluctuations, no risk of capital loss, and full financial security. Instead of withdrawing, Ravi made a smarter move—he extended his PPF for another 10 years and continued investing ₹1 lakh annually. This is where the real power of compounding came into play. Over a 25-year period, his total investment of ₹25 lakh grew to around ₹65–70 lakh. This example clearly highlights that PPF is not designed for quick or high returns, but for long-term, stable, and tax-efficient wealth creation. For a balanced financial strategy, PPF works best when combined with growth-oriented options like SIPs—where PPF provides safety and stability, while SIPs help accelerate overall wealth creation.